A valid greenhouse gas balance is the basis of any effective climate protection strategy.

All companies are requested to limit global warming by reducing their greenhouse gas emissions (GHG). Investments in climate protection are not only worthwhile for the environment and society, but also for companies. According to a study by the Potsdam Institute for Climate Impact Research (PIK), the economic damage caused by global warming is six times higher than the costs of achieving the 1.5-degree target of the Paris Climate Agreement.

Companies should therefore develop a climate strategy that aims to achieve greenhouse gas neutrality. The prerequisite for this is that they first balance their greenhouse gas emissions. This is particularly challenging for many small and medium-sized enterprises (SMEs), as creating a greenhouse gas balance is a complex process and requires considerable effort, especially the first time.

Even for companies that are not required to report according to the Corporate Sustainability Reporting Directive (CSRD), the effort for a GHG balance can be worthwhile. For business partners, financiers and consumers, the verifiable commitment of companies to climate protection is an increasingly important criterion.

Selecting the standard for GHG accounting

Before a company starts working on its greenhouse gas balance, it should first decide which methodological standard it wants to use to balance.

The most widely used standard for creating a Corporate Carbon Footprint (CCF) is the Greenhouse Gas Protocol (GHG Protocol), which defines how a company’s emissions are to be accounted for in the individual scopes. There is also a formal standard, ISO 14064. The most important difference is that a GHG report can be certified according to ISO 14064, which is not possible for the GHG Protocol. While the ISO standard primarily specifies what needs to be done, the GHG Protocol explains how to do it with instructions and guidance.

As soon as the methodological standard has been selected, GHG accounting can begin.

5 steps to the greenhouse gas balance

The GHG balance sheet for creating a Corporate Carbon Footprint (CCF)usually follows the following five steps:

The GHG balance sheet for creating a Corporate Carbon Footprint (CCF)usually follows the following five steps:

Step 1: Define organizational, operational and time boundaries

Organizational boundaries: A decision is made as to whether the balance sheet covers the entire company or only certain subsidiaries and locations. The consolidation method can be selected based on financial control, operational control or proportional consolidation.

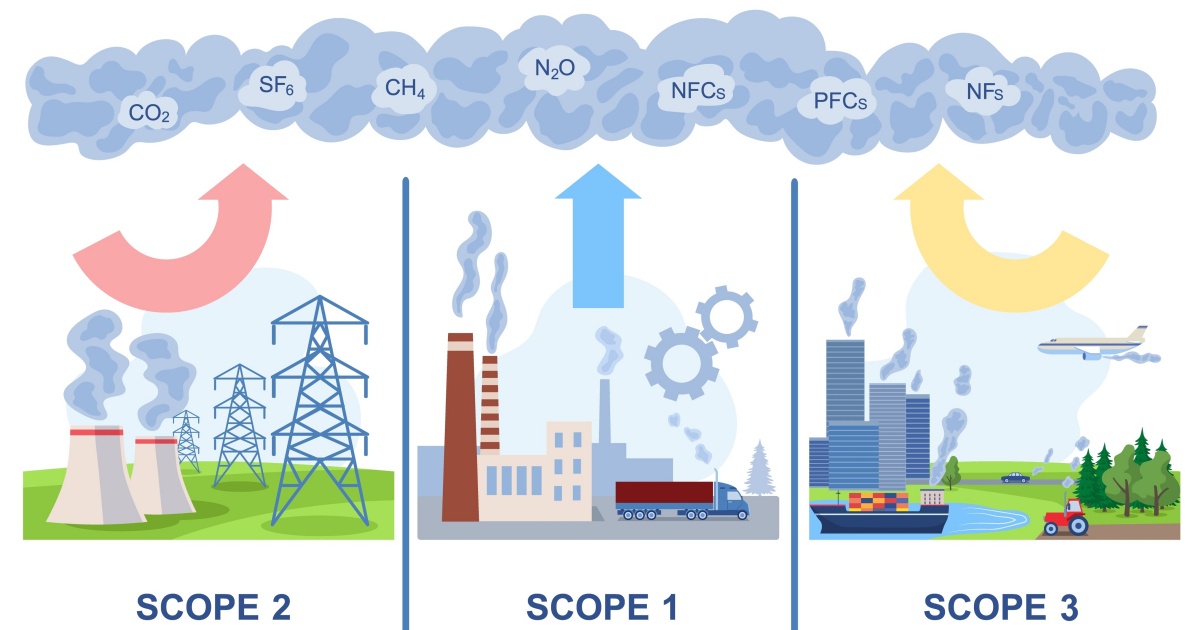

Operational boundaries: The emission sources must be defined within the defined organizational boundaries. These are divided into scope 1 (direct emissions), scope 2 (indirect energy emissions) and scope 3 (other indirect emissions from the upstream and downstream supply chain).

Specifically for Scope 3, a materiality analysis should be used to determine which emission sources have a significant impact and which can be omitted due to low materiality.

Time boundaries: The GHG balance generally refers to one year, usually a calendar year. The year of the first balance is the base year and usually serves as a reference point for reduction targets and the balances for subsequent years. Therefore, the base year should be as representative as possible and should not contain any major deviations due to exceptional external factors, such as the corona pandemic years 2020 and 2021.

Step 2: Collect activity data

Activity data document company activities that cause GHG emissions. They must be collected separately for the three scopes.

Scope 1 and 2: Collection of activity data from company-owned or controlled sources, such as vehicle fleets and heating systems (Scope 1), as well as from external sources, such as electricity and district heating (Scope 2).

Scope 3: Collection of activity data along the entire upstream and downstream value chain, e.g. for business travel, material procurement and waste management. The data must be valid, consistent and complete to enable accurate calculations of emissions.

Step 3: Determine emission factors

Emission factors are conversion factors for the activity data collected in step 2. They quantify the GHG intensity per unit of a specific activity, for example CO2 emissions per kilowatt hour of electricity consumption. Energy content and emissions released differ from energy source to energy source. Therefore, appropriate emission factors must be determined for each activity data set.

For Scope 2 and Scope 3 activities, these emission factors can be partially requested from the upstream supply chain providers. Another way is to determine emission factors from databases. Some of these databases, such as GEMIS, DEFRA and ADEME, are free of charge, others are subject to a fee.

Step 4: Calculate emissions

With the help of the determined emission factors (step 3), the collected activity data (step 2) can be converted into CO₂ equivalents (e.g. kg CO₂e per kWh).

The GHG emissions caused by the company are calculated based on the collected activity data (step 2) and determined emission factors (step 3). To do this, the activity data is multiplied by the respective individual emission factor and converted into CO₂ equivalents (e.g. kg CO₂e per kWh). The formula for this is:

GHG emissions [kg CO2e] = activity data [unit] x emission factor [kg CO2e / unit]

The resulting individual emissions are then added together. According to the GHG Protocol, individual totals must be calculated for:

- Scope 1 emissions

- Scope 2 emissions

- Scope 3 emissions

- Biogenic emissions

- GHG sinks

The sum of all emissions minus the GHG sinks, i.e. the emissions captured and bound biologically or technically, forms the total net value of GHG emissions.

Software: In principle, calculating GHG emissions is possible with standard software such as Excel. However, using specialized software can simplify the process and prevent possible miscalculations in self-made Excel tables.

Quality assurance: Regardless of the software solution chosen, the data and calculations should be checked by internal or external audits to ensure the accuracy and reliability of the calculated emissions.

Step 5: Combine results in GHG report

The results of steps 1 to 4 are combined in the fifth step in a report on the company’s GHG balance, which may be part of a more comprehensive sustainability report.

Structure and content: The report contains both qualitative and quantitative information, including a clear presentation of the methodology, the emissions determined and the associated assumptions.

Transparency and communication: The report is written and published in a form that is understandable and transparent for internal and external stakeholders.

Use greenhouse gas balance as part of the corporate climate strategy

The greenhouse gas balance is a key building block for the corporate climate strategy, which should contain the following elements:

Objective: Set concrete, measurable goals for reducing greenhouse gas emissions. These goals should be ambitious but realistic in order to advance the sustainability strategy.

Action plan: Develop a detailed plan for reducing emissions that covers various areas such as energy efficiency, renewable energy and supply chain management.

Monitoring and adaptation: Regularly review progress and adapt measures to ensure that the set goals are achieved.

These elements are based on a valid annual GHG balance, which makes it possible to develop and later review a climate strategy.

Conclusion

Companies that do not have a GHG balance or a climate strategy should start doing so as soon as possible. Otherwise, even SMEs that are not subject to reporting obligations risk competitive disadvantages. On the positive side, a GHG balance can help companies to identify their own emission patterns and identify potential for improvement and savings that go beyond GHG reduction.

If your company needs support in creating a GHG balance and developing a climate strategy, you are welcome to arrange a free, non-binding consultation with me.